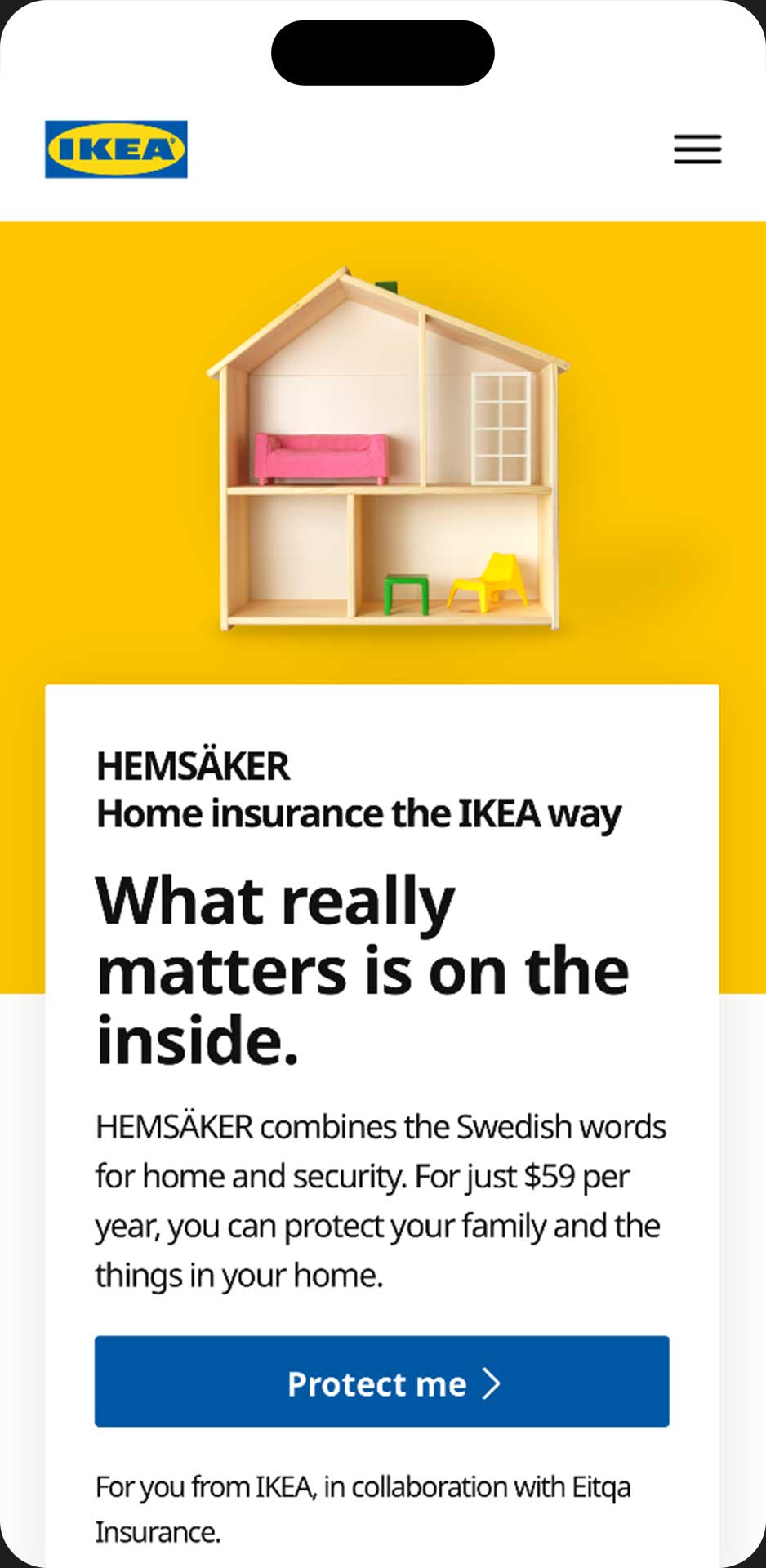

IKEA HEMSÄKER

Designing IKEA's First Insurance Product

In Brief

IKEA wanted entry into insurance without losing trust.

Brand loyalty shaped four commercial propositions.

I directed the product from concept to market-ready.

Delivery system to localise product into markets.

Proved trust can scale into regulated services.

Outcomes and Impact

10% Swiss direct market share, year one.

5x average in-store spend per claim-free year.

Top 5 CSAT in Swiss home insurance.

4 markets at launch.

Situation

A category built to resist

The home insurance category had a structural trust problem long before IKEA considered entering it. Research across IKEA's Life at Home programme, built from tens of thousands of consumers across multiple markets, showed that security was rated important or very important by 90% of respondents. It also showed that existing insurance was experienced as confusing, opaque, and built for the provider. 82% of people surveyed across Germany, Malaysia, and the US wanted something simpler and more affordable. Claiming felt like a fight. Onboarding felt like a trap. The category was not failing on features; it was failing on trust.

IKEA had spent decades building brand loyalty. The question was simple: why should IKEA do insurance? And if the answer was yes, could that trust survive a move into regulated financial products?

The brief was to design something people would actually trust.

A safer life at home is crucial to creating a better everyday life for the many people.

Approach

Insight first, product second

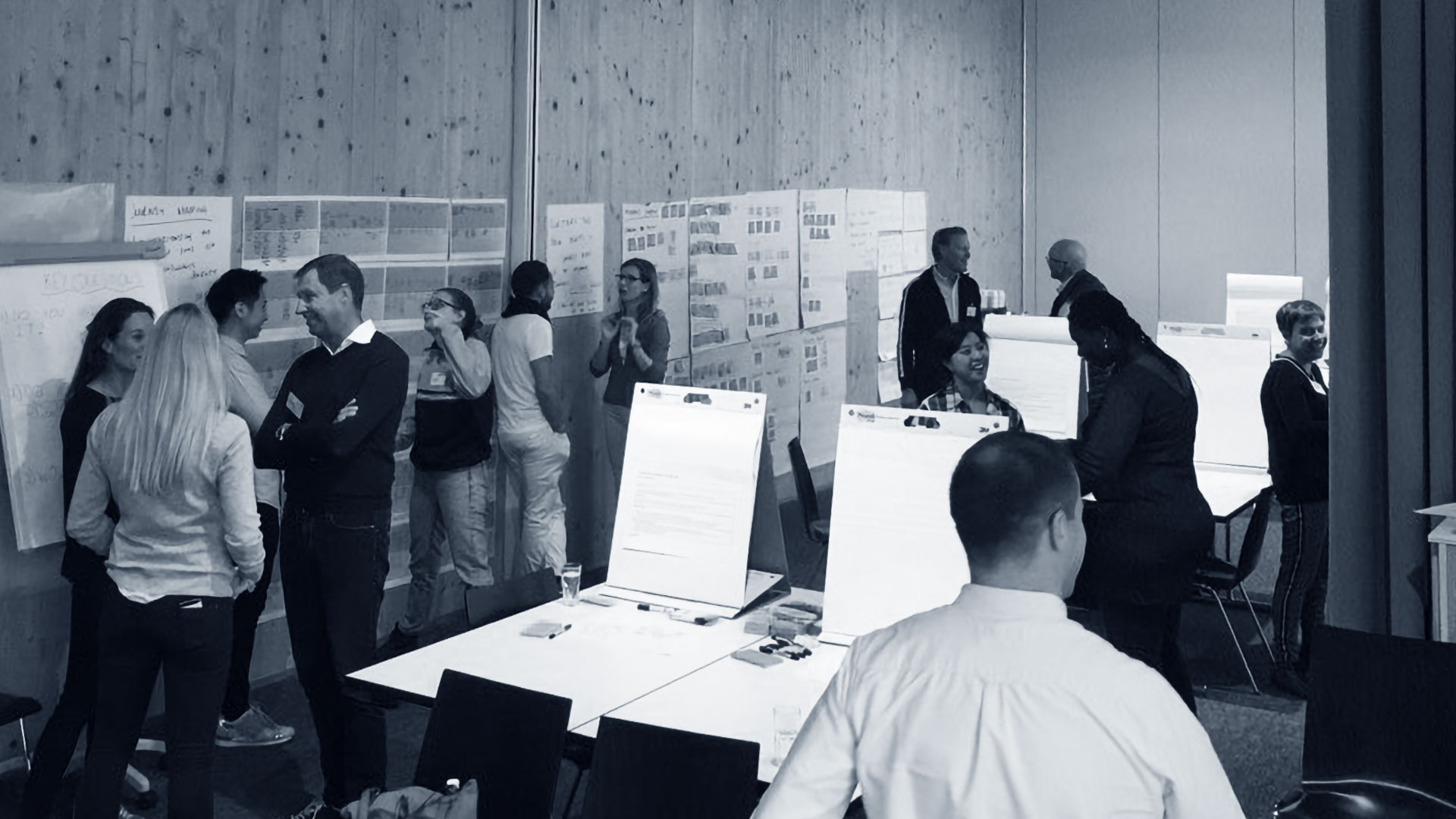

My first move was to treat the existing Life at Home research not as background, but as the brief. Working with the strategy and innovation director, I co-led a synthesis of that body of work to identify where IKEA's brand logic intersected with what people actually needed from home protection. That synthesis shaped the design of a three-day concept sprint in Switzerland, where around 30 consumers joined our multidisciplinary team alongside IKEA, Ikano Bank, and Swiss Re iptiQ executives to generate and stress-test ideas together.

The sprint structure ran on two parallel tracks. On the brand experience side, we were testing whether IKEA's plain language and democratic values could survive regulatory translation without flattening into generic insurance copy. On the customer experience side, we were mapping the specific moments where the existing category broke down: fear at the point of commitment, distrust at the point of claiming, the persistent sense that terms were written to exclude. An overnight survey of 300+ consumers validated emerging propositions across three continents in real time. By day three, four distinct concepts had been tested, refined, and taken to prototype.

Four emotional drivers had emerged from the research: safety, affordability, shared living, and sustainability. Each became the foundation for a separate proposition. Service design work ran alongside concept development, not after it, producing end-to-end journey flows, compliance logic, commercial and operational parameters in parallel with the proposition builds.

2-day synthesis session with the clients, plus 3-day hackathon with 30 consumers across different ages, lifestyles, and living situations.

System

One playbook, four markets

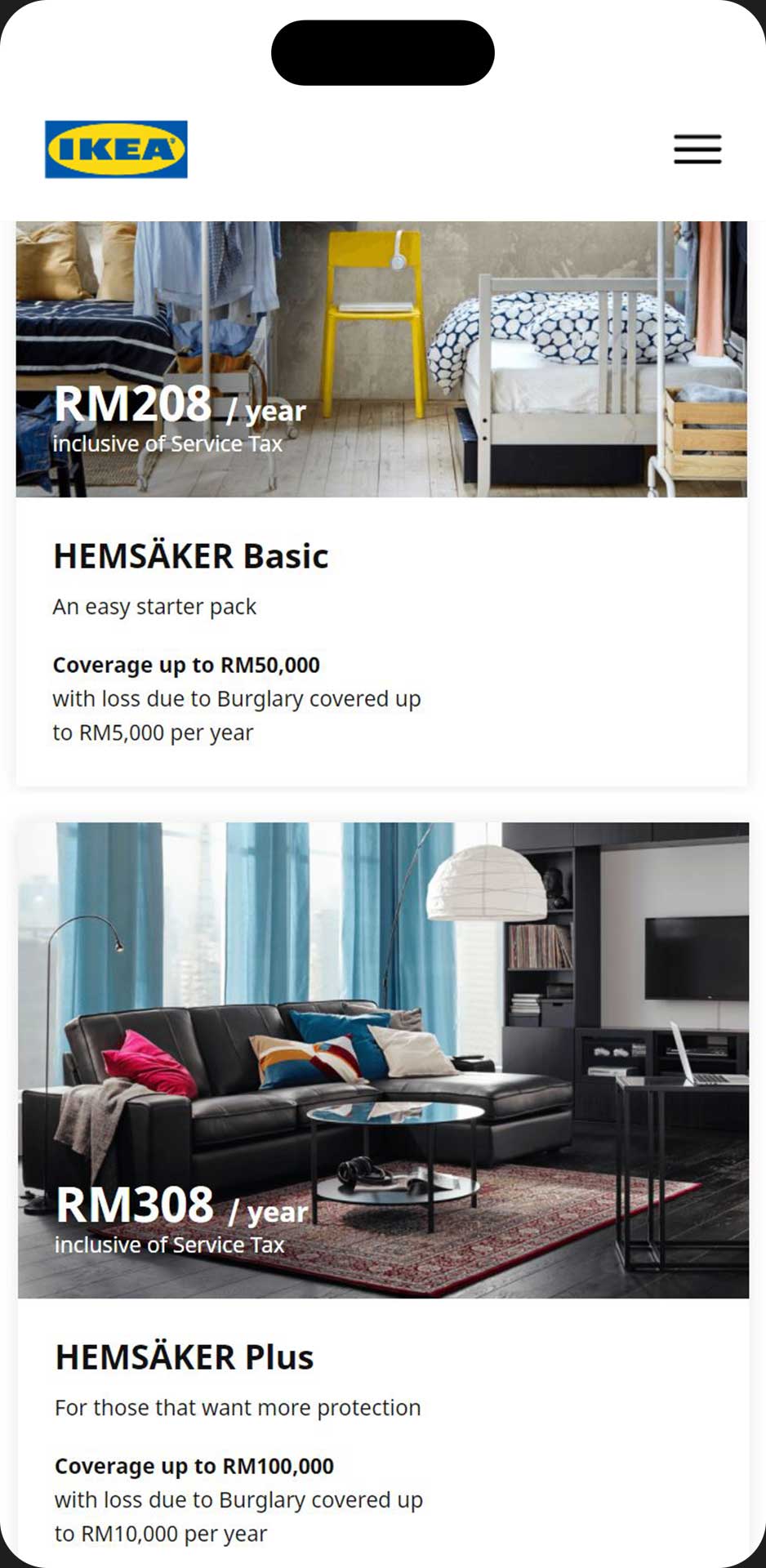

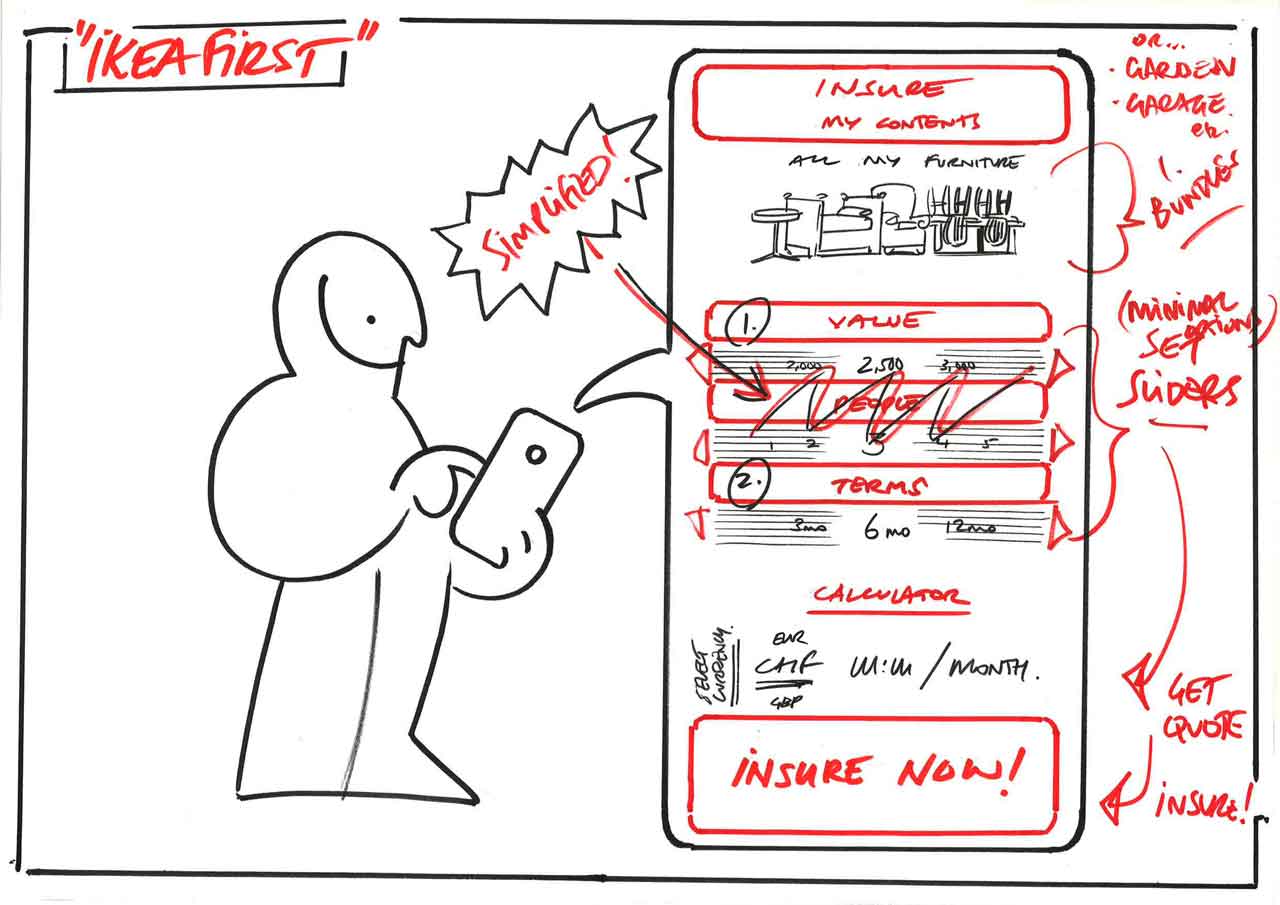

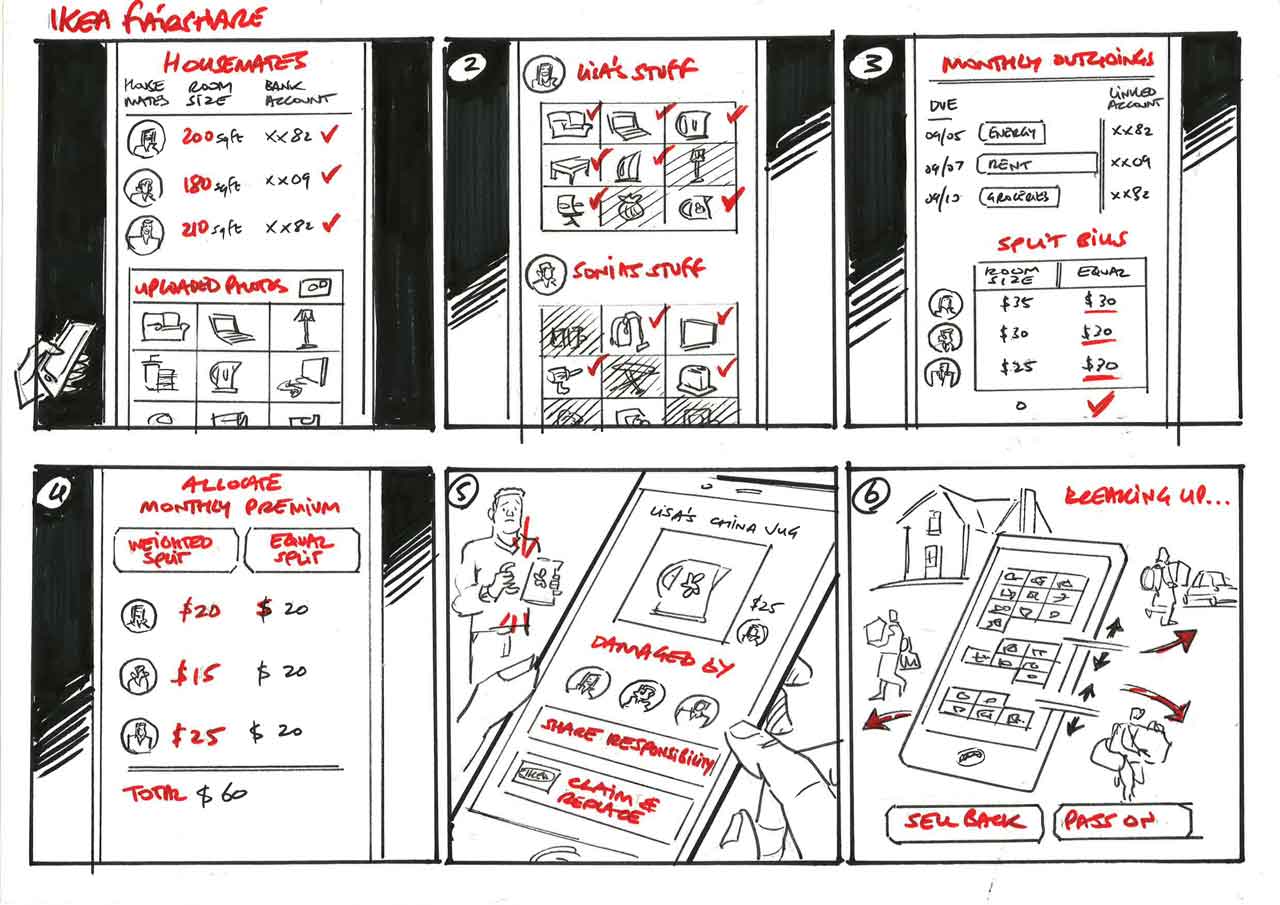

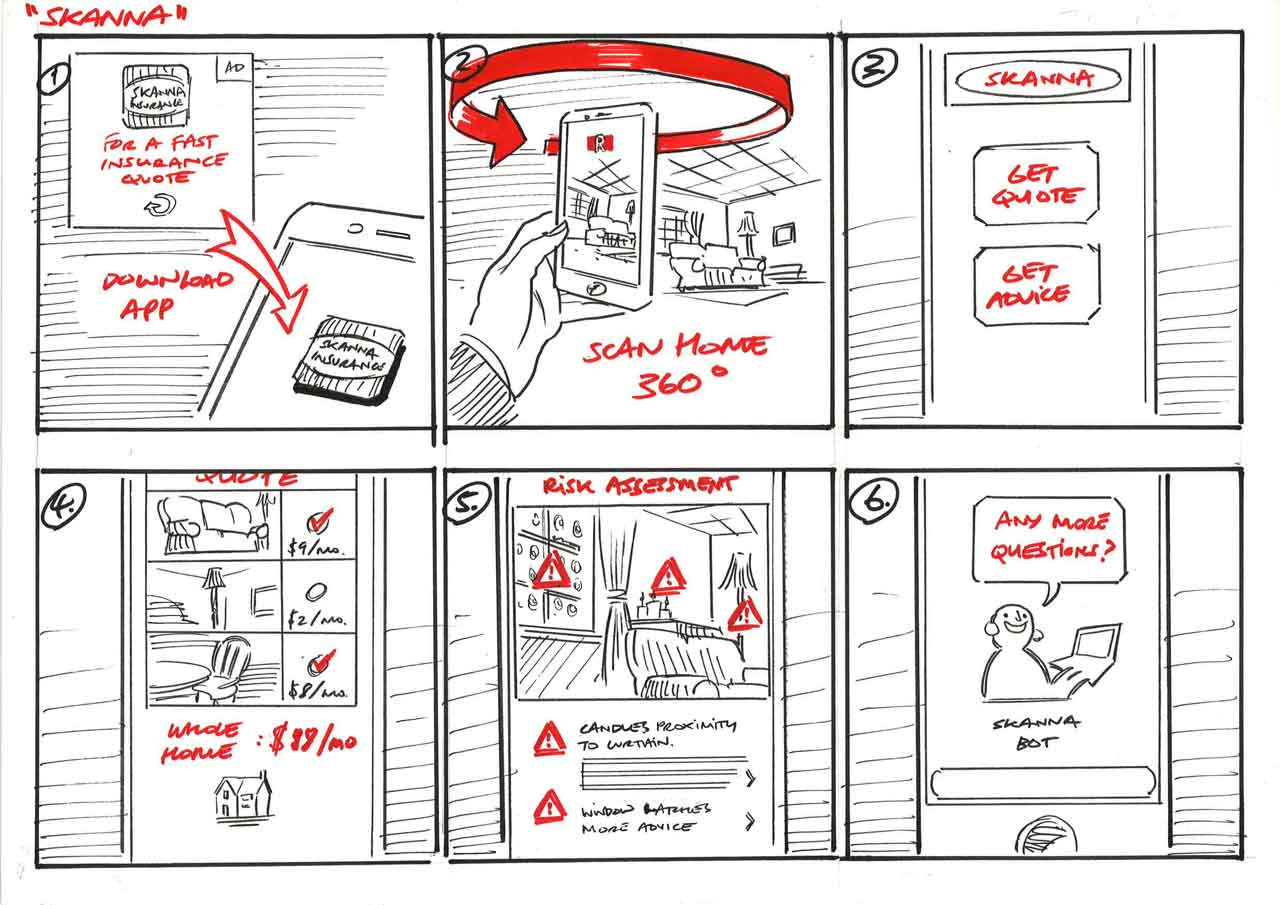

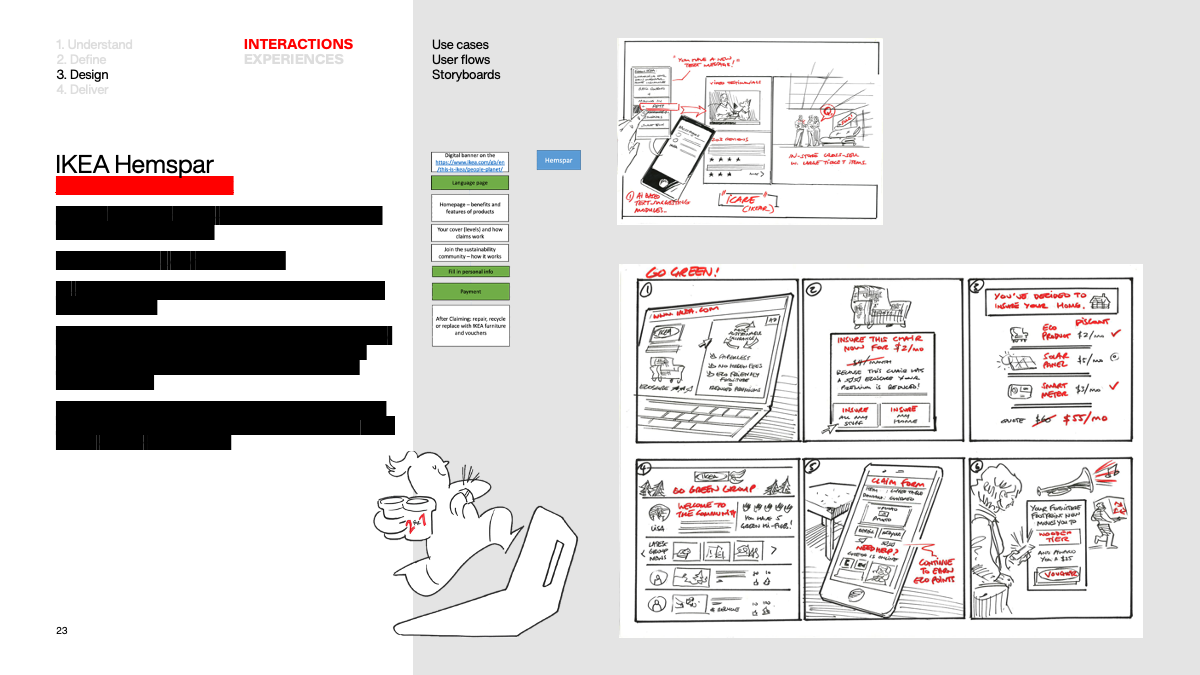

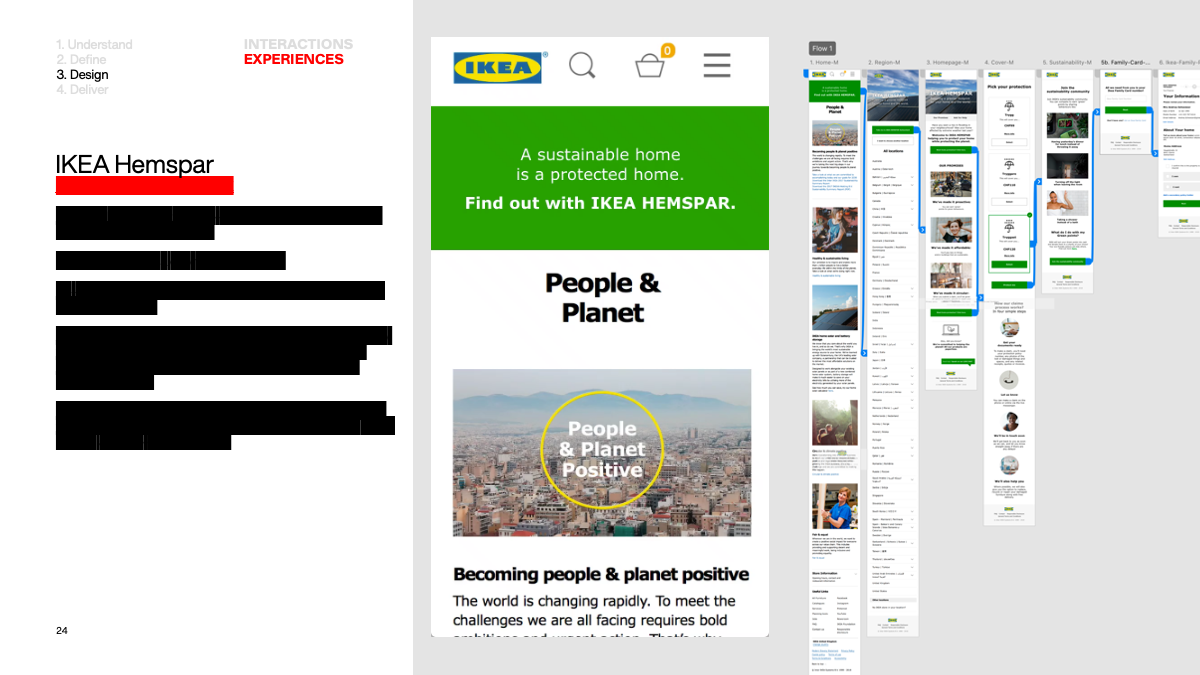

Each of the four propositions was anchored to one of those drivers and fully prototyped: user flows, service rules, marketing language, and launch assets. HEMTRYGG addressed straightforward affordability for people who wanted to understand exactly what they were buying. HEMFLEX let flatmates or partners split cost and cover. HEMSPAR rewarded eco-conscious behaviour with lower premiums and sustainability incentives. HEMSMART used home scanning to generate instant quotes and a basic safety assessment.

For each of the four concepts, the playbook codified tone of voice, journey structure, and compliance parameters (using the 4P framework) so that future markets could localise the proposition without rebuilding it from scratch. That was the system’s primary function: to make the category logic reusable, not the specific product.

The product that launched, HEMSÄKER, took HEMTRYGG as its foundation. The loyalty mechanic was simple: every claim-free year returned a CHF 20 IKEA voucher. In practice, customers spent an average of five times the voucher's face value during store visits. The brand's home association was doing real commercial work.

Ingka Group, IKEA's largest franchisee, subsequently embedded the model into its broader financial services strategy.

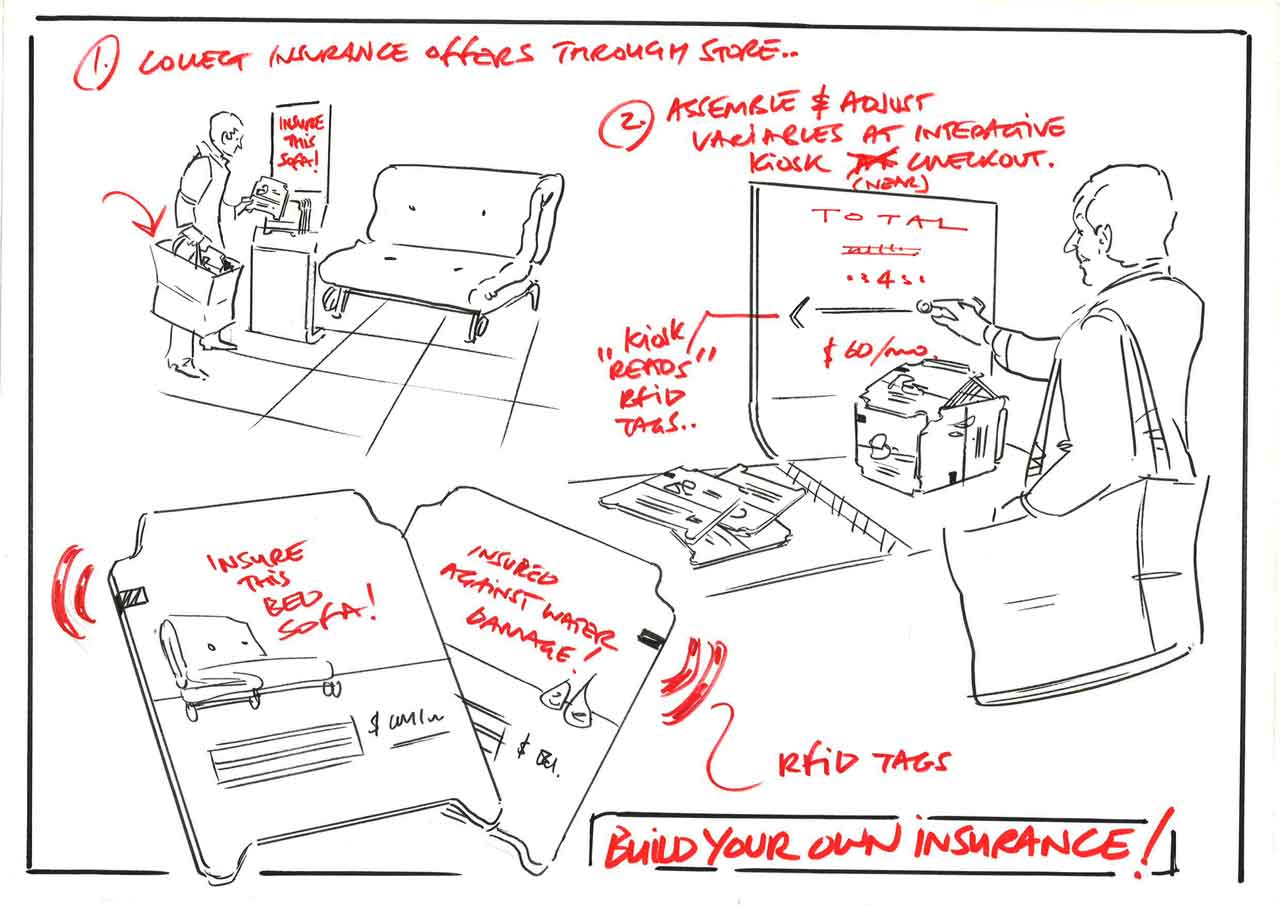

Some examples of storyboards, use cases, user flows, and concepts sketched live during the co-creation hackathon.

Some examples of product value proposition concepts.

We explored and prototyped four experience-driven product experiences aligned to different life needs.

HEMFLEX: a shared insurance plan for roommates and friends.

HEMSMART: scan your home for an instant quote and safety score.

HEMSPAR: insurance that rewards sustainable behaviour.

HEMTRYGG: simple, low-cost coverage with clear terms.

“We’re really proud of how it reflects the IKEA look and feel. It uses straight-talking language and connects naturally to the brand in a way customers understand and trust.”

Elizabeth Wesson

Digital Strategy,

Swiss Re

Outcomes

A replicable model, not just a product launch

Experience Systems turned IKEA's first move into insurance into a product that could launch, replicate, and grow. Brand experience kept IKEA's voice and values intact inside a regulated product. Customer experience turned insurance’s negatives into features people actually wanted. Service design built the logic that let four markets launch from one playbook.

10% direct market share in Switzerland, year one.

Top-5 CSAT rating, Swiss home insurance.

5x average in-store spend per claim-free year via CHF 20 voucher mechanic.

Launched across 4 markets: Switzerland, Malaysia, Singapore, Mexico.

Adopted by Ingka Group as part of IKEA's financial services roadmap.

IKEA CH: HEMSÄKER

Ikano Group: Press page

iptiQ Swiss Re: Press page

Client: IKEA, Swiss Re iptiQ, Ikano Bank

Sectors: Retail, Financial Services

Role: Director of Experience Design (C Space London)

Scope: Create - Product (BX, CX, Service Design)

Curious how this approach might apply in your context?

Call me Ale